| HOME | SEARCH | ABOUT US | CONTACT US | HELP | ||

| |

| Montana Administrative Register Notice 42-2-997 | No. 6 03/29/2019 | |

| Prev | Next | ||

|

BEFORE THE DEPARTMENT OF REVENUE OF THE STATE OF MONTANA

TO: All Concerned Persons

1. On November 2, 2018, the Department of Revenue published MAR Notice No. 42-2-997 pertaining to the public hearing on the proposed amendment and repeal of the above-stated rules at page 2193 of the 2018 Montana Administrative Register, Issue Number 21.

2. On November 26, 2018, a public hearing was held to consider the proposed amendment and repeal; no proponents or opponents were present and no oral testimony was received. The department received written comments from Tim Burton, Executive Director of the Montana League of Cities and Towns.

3. The department amends ARM 42.19.1401 and 42.19.1412, and repeals ARM 42.19.1402, 42.19.1408, 42.19.1409, 42.19.1410, and 42.19.1411 as proposed.

4. The department amends ARM 42.19.1403, 42.19.1404, and 42.19.1407 as proposed, but with the following changes from the original proposal, new matter underlined, deleted matter interlined:

42.19.1403 NOTIFICATION REQUIREMENTS FOR THE CREATION OR AMENDMENT OF AN URBAN RENEWAL DISTRICT (URD) WITH A TAX INCREMENT FINANCING PROVISION (1) remains as proposed. (2) Before the department can certify the base taxable value of property located within a newly created or amended district, the local government must notify the department of the intent to create or amend a URD containing a tax increment financing provision. The notification must include: (a) through (d) remain as proposed. (e) (f) remains as proposed. (3) If the local government wants the department to provide a list of the affected real, separately assessed improvements, personal and centrally assessed properties within the district, the local government must provide the notification information required in (2)(a) through (c), and preliminary versions of the notification information described in (2)(d) and (e), to the department no later than August 1 of the desired base year. Within 60 days after receiving the notification, the department will provide the following to the designated contact: (a) confirmation that no issues were identified with the preliminary district boundary; and (b) remains as proposed. (4) If the local government does not need the department to provide a list of the affected real, separately assessed improvements, personal and centrally assessed properties within the district, the local government must provide the notification information required in (2)(a) through (c), and preliminary versions of the notification information described in (2)(d) and (e), to the department no later than December 1 of the desired base year. (5) By no later than February 1 of the calendar year following the creation of the district, the local government must provide the department with the following: (a) final versions of the notification information described in (2)(d) and (e), if not previously provided;

(i) an effective date prior to the date on which the URD is created; (ii) the finding of blight, as required by 7-15-4210(1), MCA; and

(c) a copy of the local governing body's resolution adopting the growth policy pursuant to 76-1-604, MCA;

(e) if the documentation in (d) is not available, a copy of the document affirming that the local governing body received no written recommendation from the planning commission and scheduled the public hearing on the urban renewal plan as permitted in 7-15-4214, MCA; (d) and (e) remain as proposed but are renumbered (f) and (g).

(g) remains as proposed but is renumbered (i).

(i) remains as proposed but is renumbered (k). (6) Within 20 (a) through (7) remain as proposed.

AUTH: 15-1-201, MCA IMP: 7-15-4202, 7-15-4210, 7-15-4215, 7-15-4216, 7-15-4282, 7-15-4283, 7-15-4284, 7-15-4285, 15-10-202, 15-10-420, MCA

42.19.1404 NOTIFICATION REQUIREMENTS FOR THE CREATION OR AMENDMENT OF A TARGETED ECONOMIC DEVELOPMENT DISTRICT (TEDD) WITH A TAX INCREMENT FINANCING PROVISION (1) A local government may create or amend a TEDD containing a tax increment financing provision pursuant to Title 7, chapter 15, parts 42 and 43, MCA. The department will review a local government's urban renewal district (URD) or TEDD processes, documents, and information required under those statutes and these rules to determine fulfillment of a district's purpose and the specific requirements provided under 7-15-4279, MCA, in the department's TEDD taxable value certification process. (2) Before the department can certify the base taxable value of property located within a newly created or amended district, the local government must notify the department of the intent to create or amend a TEDD containing a tax increment financing provision. The notification must include: (a) through (d) remain as proposed. (e) (f) remains as proposed. (3) If the local government wants the department to provide a list of the affected real, separately assessed improvements, personal and centrally assessed properties within the district, the local government must provide the notification information required in (2)(a) through (c), and preliminary versions of the notification information described in (2)(d) and (e) to the department no later than August 1. Within 60 days of receiving the notification, the department will provide the following to the designated contact: (a) confirmation that no issues were identified with the preliminary district boundary; and (b) and (4) remain as proposed. (5) By no later than February 1 of the calendar year following the creation of the district, the local government must provide the department with the following: (a) final versions of the notification information described in (2)(d) and (e), if not previously provided;

(i) an effective date prior to the date on which the TEDD was created; (ii) the infrastructure deficiency finding, as required by 7-15-4280(1), MCA; and

(c) a copy of the local government's

(d) a copy of the resolution adopting the zoning of the district, pursuant to 7-15-4279, MCA; (e) a copy of the resolution adopting the growth policy, pursuant to 76-1-604, MCA, if applicable; (d) and (e) remain as proposed but are renumbered (f) and (g).

(g) and (h) remain as proposed but are renumbered (i) and (j).

(6) Within 20 (a) through (7) remain as proposed.

AUTH: 15-1-201, MCA IMP: 7-15-4279, 7-15-4282, 7-15-4283, 7-15-4284, 7-15-4285, 15-10-202, 15-10-420, 76-1-103, MCA

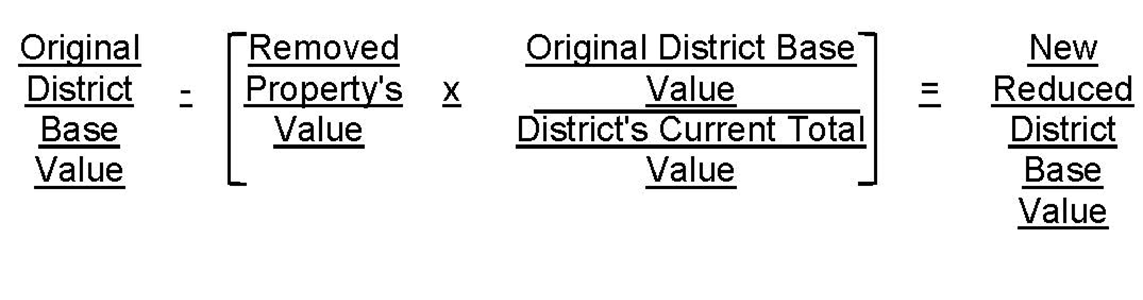

42.19.1407 DETERMINATION OF BASE AND INCREMENTAL TAXABLE VALUES OF URBAN RENEWAL DISTRICTS (URD) OR TARGETED ECONOMIC DEVELOPMENT DISTRICTS (TEDD) (1) through (4) remain as proposed. (5) A local government that amends the boundaries or makes changes within a valid URD or TEDD, pursuant to the provisions of Title 7, chapter 15, parts 42 and 43, MCA, shall follow the process described in ARM 42.19.1403 or 42.19.1404. (a) In cases where a boundary amendment removes property from an existing URD or TEDD: (i) the removed property shall be considered newly taxable pursuant to 15-10-420, MCA; (ii) the base year (iii) the total (iv) The reduced base value of the URD or TEDD will be determined by the following formula:

(b) In cases where a URD or TEDD boundary amendment adds new property to an existing URD or TEDD: (i) remains as proposed. (ii) the base taxable value of the property being added to the URD or TEDD by the boundary amendment will be the actual taxable value determined by the department for ad valorem tax purposes as of January 1 of the year in which the department (iii) and (iv) remain as proposed.

AUTH: 15-1-201, MCA IMP: 15-10-202, 7-15-4284, 7-15-4285, 15-10-420, MCA

5. The department has thoroughly considered the comments received. A summary of the comments received and the department's responses are as follows:

COMMENT 1: On behalf of the Montana League of Cities and Towns (MLCT), Mr. Burton comments that MLCT believes that the department proposes these rule amendments to collect and maintain documentation that local governments have followed the statutory requirements when creating and amending districts with tax increment financing provisions.

RESPONSE 1: The department thanks Mr. Burton for the comment. It is correct that several amendments were proposed at the recommendation of the Legislative Audit Division to require local governments to submit documentation demonstrating that they meet statutory requirements when creating and amending urban renewal districts (URD and TEDD) with tax increment financing provisions. The department and the Legislative Audit Division also agreed that updating these rules would provide better and necessary guidance to prospective and current districts relative to the department's statutory certification and reporting process for taxable property values. This revised process includes additional documentation requirements of local governments and implements more specific timelines in processing URD and TEDD paperwork so the department can certify the base taxable value of property located within a newly created or amended district.

COMMENT 2: Mr. Burton made comments regarding MLCT's interpretation of the department's statutory role in URD and TEDD districts with tax increment financing. MLCT proposed amendments to ARM 42.19.1403(2) and 42.19.1404(2) and the rules' catchphrases.

RESPONSE 2: The department appreciates the input of the MLCT and has made additional revisions to the rules' catchphrases and at ARM 42.19.1403(2) and 42.19.1404(2).

COMMENT 3: Mr. Burton stated concerns with the department's proposed amendments to ARM 42.19.1403(2)(d) and 42.19.1404(2)(d), which require a local government to provide a legal description accompanied by a map illustrating the district's proposed boundary. MLCT suggests legal descriptions may change over the course of a district's creation or amendment and proposed revisions to the amendments.

RESPONSE 3: The department appreciates the input and has made additional revisions to ARM 42.19.1403(3) through (5) and 42.19.1404(3) through (5) to address the potential for the submission of preliminary district information required under (2) in each of these rules.

COMMENT 4: Mr. Burton requests clarification or a definition for the term "geospatial vector files" in ARM 42.19.1403(2)(e) and 42.19.1404(2)(e).

RESPONSE 4: The term "geospatial vector files" refers to database files that contain spatial data models of geographic or property features which are commonly used in geographic information systems (GIS). The department has revised the amendments to clarify the industry-standard information sought by the department in GIS database files should a local government opt to provide the district property data in that form.

COMMENT 5: Mr. Burton comments that the proposed amendments to ARM 42.19.1403(3) and 42.19.1404(3), and the department's response time to provide the requested property information, will place a burden on department resources which may inadvertently result in delays in local government district projects.

RESPONSE 5: The department appreciates the comment and the MLCT's concern that the department will not be able to meet its response obligations under both rules; however, this deadline length was established at the request of the Legislative Audit Division. The department is confident that the proposed timeline can be met. The preliminary notice to the department provided in ARM 42.19.1403(3) and 42.19.1404(3) allows department staff adequate time for important preparatory work in identifying and resolving discrepancies or errors in a legal description or boundary and notifying centrally assessed taxpayers to request description and base value information, which can often take months to receive. This preparation time will enable the department to acknowledge and set up new or amended URD or TEDD districts promptly and more efficiently after all the required documentation is submitted. Notwithstanding, the department will implement the rule subsection as proposed and will monitor local government information request response times and address any complications with stakeholders should they arise.

COMMENT 6: Mr. Burton requests the purpose of the date of December 1 in ARM 42.19.1403(4) and 42.19.1404(4) for when a local government must provide the department with its district information when the entity does not need improvements and properties information within the district.

RESPONSE 6: The department thanks Mr. Burton for the comment and directs the MLCT to the second paragraph of the department's Response 5, which also applies to ARM 42.19.1403(4) and 42.19.1404(4), and to Response 3 regarding the department's additional amendments regarding preliminary district information.

COMMENT 7: Mr. Burton states that the proposed amendments under ARM 42.19.1403(5)(c) require additional revision due to the role of the municipality's planning commission, not planning board, to review and make recommendations to the local governing body regarding the urban renewal plan's conformity with the growth policy. Additional amendments were proposed.

RESPONSE 7: The department thanks Mr. Burton for the comments and agrees with the input. The department has amended ARM 42.19.1403(5)(b) through (5)(e) to include specific local government URD process requirements provided in 7-15-4210 through 7-15-4217, MCA.

COMMENT 8: Mr. Burton comments that 7-1-2122 and 7-1-4129, MCA, do not require certified mail as stated in the proposed amendments to ARM 42.19.1403(5)(f) and 42.19.1404(5)(f). MLCT requests the department revise the amendment to remove the proof of certified mailing requirement.

RESPONSE 8: The department thanks Mr. Burton for the comments and agrees with the requirement. The department has amended the content now numbered as ARM 42.19.1403(5)(h) and 42.19.1404(5)(h), respectively.

COMMENT 9: Mr. Burton commented that the department's increased role, stated in ARM 42.19.1403(6), is appreciated but concerning to MLCT if the revised processes will result in delays.

RESPONSE 9: The department appreciates the comment and concern. Based on the comment, and upon additional consideration, the department has changed the nature of the day calculation from 20 calendar days to 20 business days. The department also directs MLCT to Response 5.

COMMENT 10: Mr. Burton commented concerns with the proposed amendments under ARM 42.19.1403(6) and (6)(a), and 42.19.1404(6) and (6)(a), which seek to clarify local government timelines to respond to department requests for information and documentation used in district tax valuation certification. Amendments to provide additional local government response were proposed.

RESPONSE 10: The department thanks Mr. Burton for the comment but disagrees that the additional time proposed by MLCT for these subsections will be beneficial; and it is somewhat contrary to MLCT's concerns stated in Comment 9. The amendments to ARM 42.19.1403(6)(a) and 42.19.1404(6)(a) remain as proposed.

COMMENT 11: Mr. Burton commented on the amendments to ARM 42.19.1404(5)(c) regarding the department's proposed requirement of proof of the local government's planning board's finding that the comprehensive development plan conforms with the local government' s growth policy.

RESPONSE 11: The department thanks Mr. Burton for the comment. Based on the comments and suggested additional amendment, the department has amended ARM 42.19.1404(5)(b) to correct one statutory reference and specify in (5)(c) through(e) the local government TEDD requirements stated under 7-15-4279 and 7-15-4280, MCA, and in Title 76, chapters 1 and 2, MCA.

COMMENT 12: Mr. Burton opined that the department's amendments to ARM 42.19.1404, proposed as (5)(i), may exceed the department's rulemaking authority, and he suggested revisions to the proposed amendments.

RESPONSE 12: The department disagrees with Mr. Burton's conclusions. An agency does not exceed its rulemaking authority when, by rule, it requires copies of documents and disclosures that are evidence of other statutorily required processes or purposes. In this case, the Montana Legislature stated the purpose and requirements for TEDD districts in 7-15-4278 through 7-15-4280, MCA, and these requirements were reflected in the proposed amendments to (5)(i). The department also refers Mr. Burton and the MLCT to Response 1 as to the recommendations of the Legislative Audit Division.

Notwithstanding this general disagreement, the department believes that its role and support of the legislature's TEDD district purpose and general requirements are better stated in (1) than in (5)(i), and the department has stricken the proposed amendments in (5)(i) and amended (1) accordingly.

COMMENT 13: Mr. Burton stated that the proposed amendment under ARM 42.19.1407(5)(a)(iii) refers inaccurately to the department approving amendments to district boundaries and he proposed revisions to the proposed rule amendments.

RESPONSE 13: The department appreciates the comments and agrees that the proposed rule text requires additional amendment to clarify the impact that an amendment to a URD or TEDD district has on base, incremental, and total taxable values. Based on the comments, the department has amended ARM 42.19.1407(5) by clarifying language for the various types of values discussed in URD or TEDD certification and provides the formula that the department will use when it processes and certifies a local government's amendments to a URD or TEDD.

/s/ Todd Olson /s/ Gene Walborn Todd Olson Gene Walborn Rule Reviewer Director of Revenue

Certified to the Secretary of State March 19, 2019.

|

A directory of state agencies is available online at http://www.mt.gov/govt/agencylisting.asp.

For questions about the organization of the ARM or this web site, contact [email protected].